Created: 2026-05-14

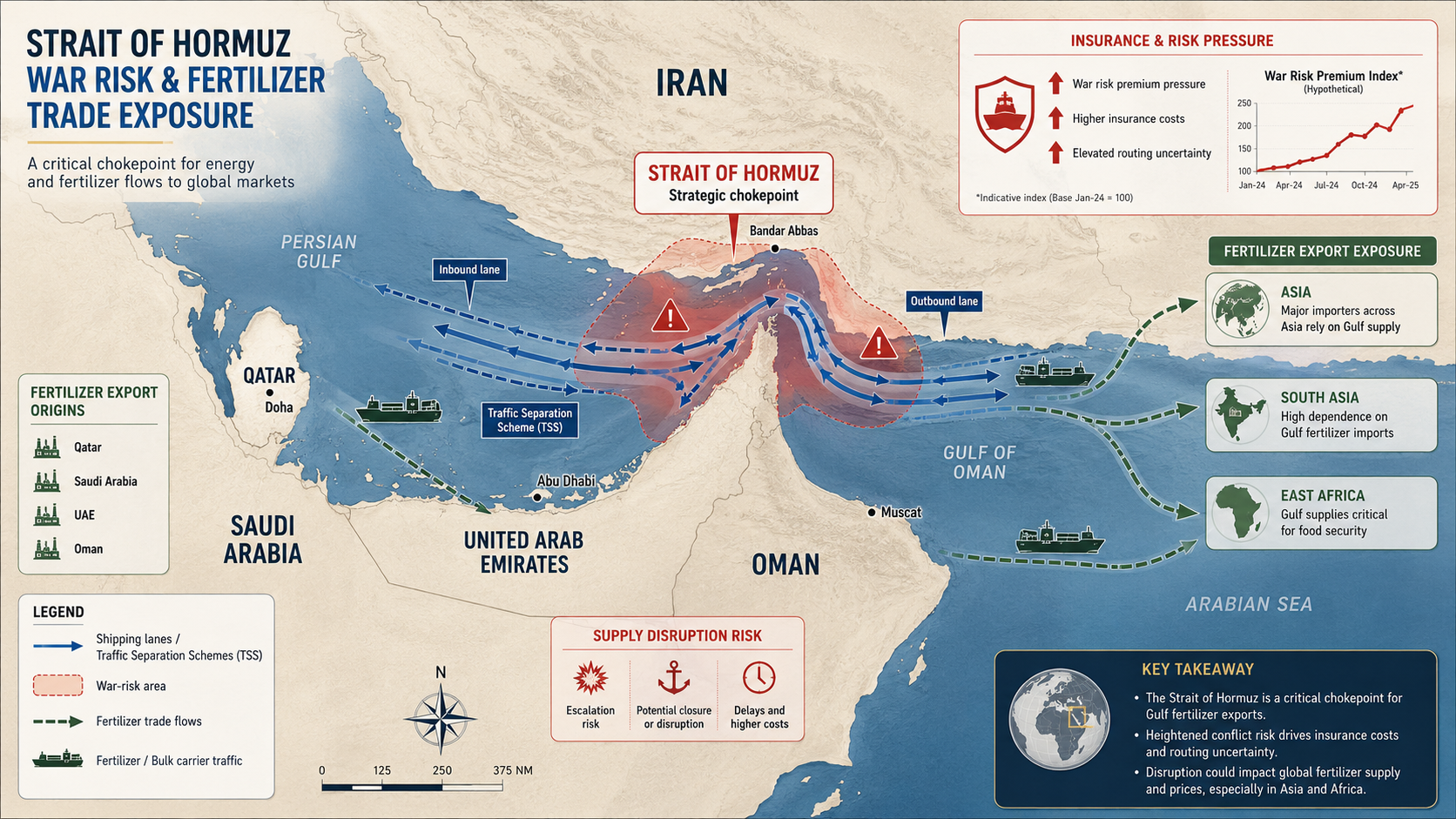

The Strait of Hormuz has moved beyond a conventional energy chokepoint story. In May 2026, it has become a live test of maritime security, marine insurance capacity, freight economics and supply-chain resilience. The latest JMIC and UKMTO updates still describe traffic through the Strait as significantly reduced, with mine risk in and near the Traffic Separation Scheme and sporadic GNSS interference remaining part of the operating environment.

Under normal conditions, the Strait of Hormuz is one of the world’s most critical energy arteries. The IEA estimates that around 20 million barrels per day of crude oil and oil products passed through the Strait in 2025, equal to roughly one quarter of global seaborne oil trade. The same corridor also carries almost 20% of global LNG trade through exports from Qatar and the UAE.

The immediate operational issue is not whether one or two vessels can pass. The issue is whether commercial traffic can resume at scale under predictable rules of navigation, security and insurance. JMIC Advisory Note 004-26 said vessels choosing to transit should consider routing via Oman territorial waters south of the Traffic Separation Scheme, while transit via or close to the TSS should be considered extremely hazardous because of mine threats that had not been fully surveyed and mitigated.

The legal and insurance dimension is equally important. The Joint War Committee, a Lloyd’s and London market body, publishes Listed Areas where vessels are considered exposed to higher war-related perils. Ships entering those areas may need additional war risk coverage, while pricing remains a matter for negotiation between underwriters and brokers.

The current JWC update, JWLA-033, dated 2026-03-03, added Bahrain, Djibouti, Kuwait, Oman and Qatar to the Listed Areas and amended the defined area covering the Persian/Arabian Gulf, Gulf of Oman, Indian Ocean, Gulf of Aden and Southern Red Sea. This is why Lloyd’s JWC listed areas Hormuz in 2026 is highly relevant for shipowners, charterers, insurers and commodity traders.

War risk premium is now a direct cost variable rather than a back-office insurance detail. Reuters reported in March that a 3% war-risk rate on a tanker valued at USD 250 million would imply about USD 7.5 million of hull war-risk premium, compared with around 0.25%, or USD 625,000, before the conflict. Broker comments cited by Reuters also indicated that rates were changing daily and depended on vessel type, location, flag, cargo and other specific risk factors.

Argus reported that additional war risk premium levels for tankers and bulk carriers stood around 1% on 2026-04-13, with a 35-50% no-claim bonus applied to vessels remaining in the Mideast Gulf. It also reported indicative AWRP levels of around 0.5% for the Gulf of Oman and 0.75% for Bab el-Mandeb, while Hormuz itself remained more difficult to insure, including a 3% single-passage quote that was later withdrawn.

A key nuance is that insurance availability and operational safety are not the same thing. The Lloyd’s Market Association stated in March that war insurance remained available in the Lloyd’s and London company market, but that reduced vessel traffic was driven primarily by safety concerns for crew and vessels, not by a complete absence of insurance capacity.

For commodity markets, the risk transmission is mechanical. Reduced transit capacity raises freight costs, delays cargo arrival, increases demurrage and inventory costs, and changes the economics of alternative sourcing. The IEA reported that crude and oil product flows through Hormuz plunged from around 20 mb/d before the war to just over 2 mb/d in March, while alternative routes through Saudi Arabia’s west coast and the UAE’s Fujairah increased but remained insufficient to fully offset the disruption.

Effect on fertiliser market is even bigger than on crude oil

UNCTAD has warned that the Strait carries significant fertilizer volumes, while freight rates, war-risk premiums and marine fuel costs are all rising. It also estimates that around one third of global seaborne fertilizer trade, about 16 million tonnes, passes through the Strait.

IFA data add more detail. In 2024, Iran, Qatar, Saudi Arabia, the UAE and Bahrain together accounted for 23% of global ammonia trade, 34% of global urea trade and 18% of global ammoniated phosphate trade. IFA also said nearly 18.5 million tonnes of urea were exported via the Strait of Hormuz in 2024, while almost half of global sulfur trade moved through the same route.

This makes the GCC fertilizer market a second-order shock channel. The first shock is shipping and insurance. The second is fertilizer availability and affordability. The third is crop yield risk, because fertilizer applications are tied to crop calendars and cannot simply be postponed without production consequences. FAO warned in May that fertilizer scarcity linked to Hormuz disruptions could reduce yields and tighten food supplies in late 2026 and into 2027.

For market participants, the practical monitoring framework should combine five indicators: JMIC and UKMTO advisory language, JWC Listed Area changes, additional war risk premium quotes, AIS-visible transit counts, and physical availability of alternative export routes. A fall in premiums without a sustained increase in vessel movements would not be enough to confirm normalisation.

The base case is not an immediate return to pre-conflict routing economics. Even if isolated transits continue, the market needs evidence of sustained safe passage, credible mine-risk mitigation, stable naval coordination, predictable underwriting terms and normal vessel density. Until then, Hormuz remains a live risk premium across energy, freight, insurance and fertilizers.

What is the JMIC advisory for the Strait of Hormuz in May 2026?

JMIC and UKMTO updates in May 2026 describe Strait of Hormuz traffic as significantly reduced, with mine risk near the Traffic Separation Scheme and sporadic GNSS interference still relevant to vessel operators.

What are Lloyd’s JWC Listed Areas?

The Joint War Committee publishes Listed Areas where vessels are considered exposed to increased war-related perils. Vessels trading into these areas may need additional war risk cover, with pricing negotiated between brokers and underwriters.

How much are Strait of Hormuz war risk premiums in 2026?

There is no universal price. Reuters reported indicative levels around 1-1.5% of vessel value in March, with a 3% example implying about USD 7.5 million for a USD 250 million tanker. Argus later reported around 1% AWRP for tankers and bulkers in the Mideast Gulf, with Hormuz-specific quotes more difficult and volatile.

Why would reopening the Strait not immediately reduce insurance costs?

Insurance pricing depends on predictable safety conditions, not just formal navigability. Underwriters need evidence of sustained safe transit, reduced mine risk, fewer seizures or attacks, and stable rules of engagement.

Why does the Strait of Hormuz matter for fertilizers?

The Middle East is a major exporter of ammonia, urea, ammoniated phosphates and sulfur. IFA says nearly 18.5 million tonnes of urea were exported via Hormuz in 2024, and FAO warns that delayed fertilizer access can affect harvests into late 2026 and 2027.

Sources reviewed:

This article is based on a review of official maritime security advisories, insurance market updates, energy flow data, fertilizer trade analysis and market reporting.

Primary sources reviewed include JMIC and UKMTO advisories on the Strait of Hormuz operating environment, IMO maritime security communications, Lloyd’s Market Association and International Underwriting Association materials on the Joint War Committee and Listed Areas, IEA analysis of oil and LNG flows through the Strait of Hormuz, UNCTAD commentary on shipping and supply-chain exposure, FAO analysis of fertilizer scarcity and food-security risks, IFA data on fertilizer trade flows, and market reporting from Reuters and Argus on war-risk premiums, insurance availability and freight implications.

The article separates confirmed source-based information from market interpretation. Insurance premium levels are indicative and may vary materially by vessel type, flag, cargo, voyage, underwriting capacity, route, timing and broker negotiation. The operational situation in the Strait of Hormuz can change quickly, so readers should verify current JMIC, UKMTO, JWC and insurer guidance before making commercial, chartering or insurance decisions.