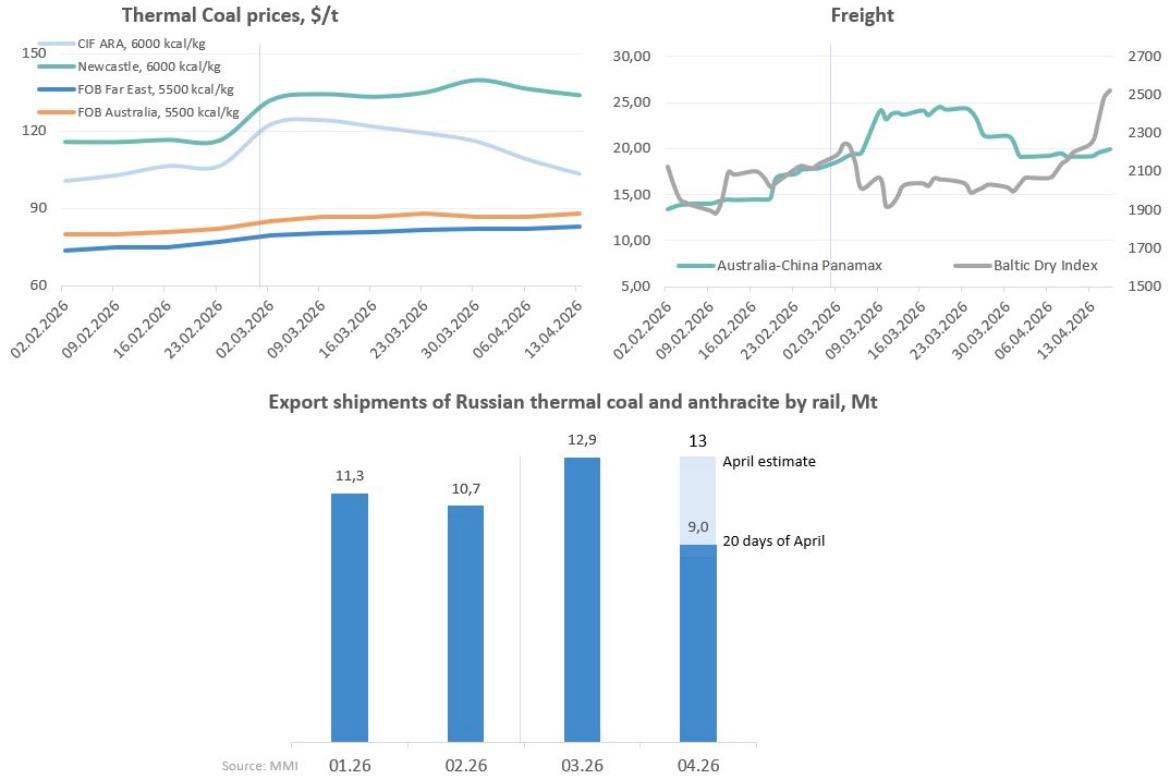

With the outbreak of the military conflict in the Middle East, thermal coal prices rose in March in both Europe (+17%) and Asia (+8-15%; FOB freight rates limited the increase). However, in April, the trend changed: prices in Europe began to decline, almost returning to the February level, while prices for high-calorie coal in Asia decreased only slightly, and prices for coal with a calorific value of 5,000-5,500 kcal/kg continued to rise gradually.

The off-season in Europe, stable renewable production, and "delayed" demand for LNG due to concerns about stockpiling for the next winter were the main reasons for the drop in energy prices in April. The process of decommissioning coal-fired power plants in the EU has been challenging, with most measures focused on delaying the closure rather than increasing actual generation in the here-and-now. At the same time, LNG prices may rise by June due to uncertain prospects for the operation of the Strait of Hormuz, and U.S. supplies may not be able to fully replace Qatari LNG.

In the JKT region, countries have quickly taken practical measures to potentially increase coal generation. South Korea has lifted its 80% capacity limit on coal-fired power plants, and there have been reports of potential reductions in sulfur requirements for imported thermal coal. Japan allowed inefficient coal-fired power plants with an efficiency of less than 42% to resume operations for one year, after which new requests for annual supply contracts were received from companies. A certain shortage of supplies from Indonesia provided additional support. The slight decrease in prices for high-calorie coal was due to positive expectations for peace negotiations and the absence of new attacks on LNG infrastructure in the Middle East.

At the same time, the dynamics of coal prices in the 5000-5500 kcal/kg segment may more accurately reflect the underlying situation in Asian energy markets amid ongoing tensions in the Strait of Hormuz. Unlike the high-calorie segment, which is more sensitive to short-term news, prices in the 5000-5500 kcal/kg segment have continued to rise gradually. Demand in India and Southeast Asia is expected to remain strong until the onset of the monsoon season, while demand in China is already beginning to recover before the summer season.

Russian exporters increased coal shipments by rail significantly in March, predominantly to ports in the Far East. Shipments will remain high in April and are likely to remain close to March levels by the end of the month. Despite ongoing domestic restrictions, price increases and the diversion of Australian coal supplies to markets closed to Russia may allow exporters to increase shipments to South Korea, China, India and Vietnam.

As summer approaches, the ongoing uncertainty surrounding the military conflict in the Middle East will inevitably continue to impact energy markets.

The off-season in Europe, stable renewable production, and "delayed" demand for LNG due to concerns about stockpiling for the next winter were the main reasons for the drop in energy prices in April. The process of decommissioning coal-fired power plants in the EU has been challenging, with most measures focused on delaying the closure rather than increasing actual generation in the here-and-now. At the same time, LNG prices may rise by June due to uncertain prospects for the operation of the Strait of Hormuz, and U.S. supplies may not be able to fully replace Qatari LNG.

In the JKT region, countries have quickly taken practical measures to potentially increase coal generation. South Korea has lifted its 80% capacity limit on coal-fired power plants, and there have been reports of potential reductions in sulfur requirements for imported thermal coal. Japan allowed inefficient coal-fired power plants with an efficiency of less than 42% to resume operations for one year, after which new requests for annual supply contracts were received from companies. A certain shortage of supplies from Indonesia provided additional support. The slight decrease in prices for high-calorie coal was due to positive expectations for peace negotiations and the absence of new attacks on LNG infrastructure in the Middle East.

At the same time, the dynamics of coal prices in the 5000-5500 kcal/kg segment may more accurately reflect the underlying situation in Asian energy markets amid ongoing tensions in the Strait of Hormuz. Unlike the high-calorie segment, which is more sensitive to short-term news, prices in the 5000-5500 kcal/kg segment have continued to rise gradually. Demand in India and Southeast Asia is expected to remain strong until the onset of the monsoon season, while demand in China is already beginning to recover before the summer season.

Russian exporters increased coal shipments by rail significantly in March, predominantly to ports in the Far East. Shipments will remain high in April and are likely to remain close to March levels by the end of the month. Despite ongoing domestic restrictions, price increases and the diversion of Australian coal supplies to markets closed to Russia may allow exporters to increase shipments to South Korea, China, India and Vietnam.

As summer approaches, the ongoing uncertainty surrounding the military conflict in the Middle East will inevitably continue to impact energy markets.