Updated: 19 May 2026

The Abu Dhabi Crude Oil Pipeline, better known as ADCOP or the Habshan-Fujairah pipeline, has become one of the most important pieces of energy infrastructure in the Gulf. For commodity traders, shipping companies, bunker buyers and risk managers, ADCOP is not just a pipeline. It is a physical option on Gulf crude export risk.

The reason is simple: most Gulf oil exports are structurally exposed to the Strait of Hormuz, while ADCOP allows part of the UAE’s crude to move directly from Abu Dhabi to Fujairah on the Gulf of Oman, outside the Strait.

But the key market point is often misunderstood. ADCOP is a partial bypass, not a full substitute for Hormuz. The commercial question is not "does the UAE have a pipeline that bypasses the Strait of Hormuz?" It does. The real questions are: how much crude can it move, which grades can it move, whether Fujairah can load reliably, and how the same disruption affects bunker fuel, tanker availability and freight cost

What is ADCOP?

ADCOP stands for Abu Dhabi Crude Oil Pipeline. According to ADNOC, Abu Dhabi Crude Oil Pipeline LLC is 100% owned by ADNOC and owns an approximately 406 km pipeline carrying crude oil from an ADNOC Onshore collection centre in Abu Dhabi to the Fujairah oil export terminal. ADNOC says the pipeline gives access to international shipping routes and allows a significant proportion of UAE crude production to be transported directly to the Arabian Sea

Public sources describe the same asset with slightly different length figures. ADNOC refers to approximately 406 km, the Port of Fujairah refers to a 360 km ADNOC crude oil pipeline, and the IEA rounds the route to around 400 km. For market analysis, the economically relevant variables are not the exact kilometre count, but capacity, utilization, terminal reliability and available export headroom.

In practical terms, ADCOP moves crude from the Abu Dhabi onshore system to Fujairah, where cargoes can be loaded without passing through the Strait of Hormuz. Reuters describes ADCOP as the Habshan-Fujairah pipeline that transports oil from Abu Dhabi’s fields to Fujairah, with Fujairah loading the UAE’s Murban crude grade, sold mostly to Asian buyers.

Why ADCOP matters now

The Strait of Hormuz remains one of the world’s most systemically important energy chokepoints. The IEA estimates that in 2025 nearly 20 million barrels per day of oil moved through the Strait, including nearly 15 million barrels per day of crude oil and condensate and around 5 million barrels per day of oil products. Around 80% of oil transiting the Strait was destined for Asia.

This matters because a disruption in Hormuz is not just a shipping issue. It can affect crude flows, product flows, LNG, bunker fuel, tanker positioning, insurance premiums, demurrage risk and ultimately delivered commodity prices.

The IEA’s key conclusion is that alternative routes are limited. Only Saudi Arabia and the UAE have operational crude pipelines that can potentially reroute flows to bypass Hormuz, with estimated available capacity of 3.5 to 5.5 million barrels per day across Saudi and UAE routes. This is material, but still far below the roughly 20 million barrels per day of oil that normally moves through the Strait

That is why ADCOP should be treated as a strategic constraint reducer, not as a complete hedge.

ADCOP capacity: nameplate, reported capacity and spare headroom

The most important number for traders is capacity.

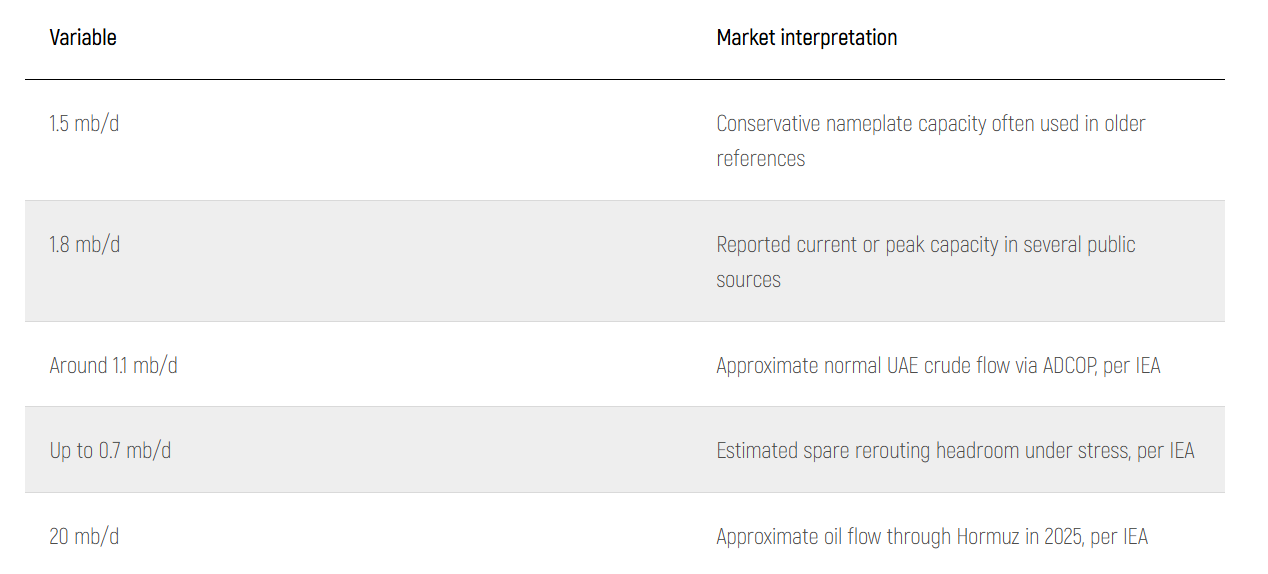

The IEA states that ADCOP’s original nameplate capacity is 1.5 million barrels per day, with reported current capacity close to 1.8 million barrels per day. It also estimates that the UAE exports around 1.1 million barrels per day of domestic crude through this route, leaving room for up to roughly 700,000 barrels per day of additional volumes in a Strait closure scenario.

The Port of Fujairah also states that the ADNOC crude pipeline has been pumping crude since 2012 and has transmission capacity of 1.8 million barrels per day.

For a trader, the useful framework is:

This is the central analytical point: ADCOP can materially improve the UAE’s export resilience, but it cannot neutralise a full Hormuz disruption for the region.

How the UAE bypasses the Strait of Hormuz

ADCOP bypasses Hormuz by connecting Abu Dhabi’s onshore crude system to Fujairah, located on the Gulf of Oman. Unlike terminals inside the Gulf, Fujairah gives tankers access to open-water routes without first transiting the Strait

This creates three forms of optionality.

First, it gives ADNOC an alternative crude export outlet. Second, it increases Fujairah’s importance as a storage, blending and bunkering hub. Third, it creates a pricing distinction between Gulf barrels that are trapped behind Hormuz and barrels that can reach international buyers through non-Hormuz infrastructure.

For crude traders, this distinction can affect grade differentials, destination optionality and the implied value of cargoes deliverable outside the Strait. For tanker operators, it can change voyage planning, bunker procurement, war-risk premia and port rotation. For industrial buyers in Asia, it can affect which Gulf suppliers remain operational during a chokepoint event.

Fujairah is the bottleneck, not just the exit point

ADCOP’s strategic value depends on Fujairah. A pipeline that reaches a constrained or disrupted export terminal is not the same as usable export capacity.

Fujairah is a major oil hub. Reuters reports that the port has around 18 million cubic metres of storage capacity and is one of the world’s top hubs for crude, fuels and blending operations, with major storage companies including VTTI, Vitol, ADNOC and Vopak.

The Port of Fujairah describes Fujairah as one of the world’s three largest bunkering hubs. Bunker fuels are stored mainly at liquid bulk terminals in FOIZ, loaded at FOTT and supplied by bunker barges to the Fujairah Anchorage Area.

This means Fujairah is not only a crude export outlet. It is also a bunker fuel hub, a product storage hub and a blending location. In a Gulf disruption scenario, these functions become correlated. A problem at Fujairah can affect crude loading, bunker fuel availability and freight execution at the same time.

Marine fuel shortages: the hidden transmission channel

Oil market commentary usually focuses on crude price. Freight operators often care more about bunker availability and bunker price.

S&P Global reported that Fujairah heavy distillate stocks, used as ship fuel and for power generation, fell to an all-time low of 2.822 million barrels in early May 2026. The same report assessed Fujairah marine fuel 0.5% sulfur at $950 per metric ton on 5 May 2026, after reaching $1,126 per metric ton on 12 March, the highest since July 2022.

For logistics operators, this is not a secondary issue. Higher bunker prices directly raise voyage cost. Tight availability increases waiting time, substitution risk and schedule uncertainty. For dry bulk, container and tanker operators, a bunker squeeze around Fujairah can transmit Hormuz risk into freight even when the vessel itself does not transit Hormuz.

This is why the operational market dashboard should include not only Brent, Murban and tanker rates, but also:

- Fujairah bunker availability by grade

- VLSFO and HSFO price differentials versus Singapore

- Fujairah oil product inventory data

- Vessel waiting times and bunker barge availability

- War-risk insurance and P&I restrictions

- Actual crude loading performance at Fujairah

ADCOP and the UAE’s post-OPEC export flexibility

The UAE announced that it would exit OPEC and OPEC+ effective 1 May 2026, citing its long-term energy strategy, production policy and future capacity. WAM described the decision as part of the UAE’s move to enhance flexibility and respond to market dynamics.

Separately, ADNOC states that it plans to increase lower-carbon hydrocarbon production capacity to 5 million barrels per day by 2027

For the market, the important issue is the difference between production capacity and export capacity. Higher upstream capacity only matters to international buyers if barrels can reach the market. ADCOP gives the UAE a strategic advantage over Gulf producers without meaningful non-Hormuz export routes, but the pipeline’s current capacity is still finite.

Argus noted that the UAE can bypass Hormuz using the 1.5 million barrels per day ADCOP pipeline, but also argued that near-term supply flows remain constrained by Strait disruptions regardless of quota structures.

That is the right market interpretation. UAE production flexibility is more valuable when logistics are open. Under a severe Hormuz or Fujairah disruption, the binding constraint can shift from reserves and wells to pipeline capacity, terminal capacity, storage and vessel access.

Is BlackRock an ADCOP owner?

This is a common search query, but it needs careful wording.

There was a separate major ADNOC oil pipeline infrastructure transaction in 2019 involving BlackRock, KKR, GIC and Abu Dhabi Retirement Pensions and Benefits Fund. ADNOC said the combined investment in select ADNOC oil pipeline infrastructure reached $4.9 billion, with BlackRock and KKR together holding 40%, ADRPBF 3%, GIC 6% and ADNOC 51% in ADNOC Oil Pipelines LLC. ADNOC also stated that sovereignty over the pipelines and management of pipeline operations remained with ADNOC.

Therefore, for SEO and factual accuracy, the clean answer is:

BlackRock participated in ADNOC oil pipeline infrastructure investment, but public ADNOC materials identify ADCOP itself as 100% owned by ADNOC. Do not state that BlackRock owns ADCOP unless a specific official document for ADCOP proves that claim.

BlackRock participated in ADNOC oil pipeline infrastructure investment, but public ADNOC materials identify ADCOP itself as 100% owned by ADNOC. Do not state that BlackRock owns ADCOP unless a specific official document for ADCOP proves that claim.

ADCOP expansion: what should traders assume?

There is market interest in a possible expansion of UAE bypass capacity, including references to a potential Jebel Dhanna to Fujairah pipeline. Industry reporting has discussed additional pipeline capacity, but for risk models the conservative approach is to treat only currently operational, verifiable capacity as available.

As of 14 May 2026, the most defensible assumption for a trading or logistics model is:

Base case: ADCOP available capacity is 1.5 to 1.8 mb/d.

Stress case: usable capacity is lower if Fujairah terminal operations, storage, pumping, security or vessel access are constrained.

Upside infrastructure case: additional UAE bypass capacity may become relevant only after official confirmation of commissioning and sustained export performance.

Base case: ADCOP available capacity is 1.5 to 1.8 mb/d.

Stress case: usable capacity is lower if Fujairah terminal operations, storage, pumping, security or vessel access are constrained.

Upside infrastructure case: additional UAE bypass capacity may become relevant only after official confirmation of commissioning and sustained export performance.

This distinction matters because paper capacity is not the same as deliverable barrels. A pipeline expansion does not fully de-risk the system until it has been tested through actual crude nominations, terminal throughput, storage handling and vessel loading.

Practical implications for commodity traders

For crude traders, ADCOP changes the UAE’s risk profile relative to other Gulf exporters.

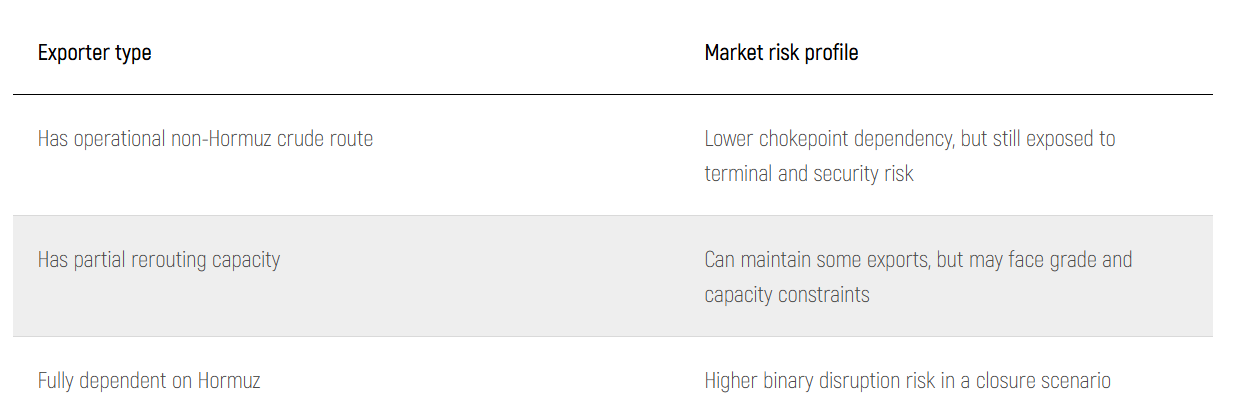

A buyer comparing Gulf suppliers should separate exporters into three buckets:

The UAE belongs in the second category: it has meaningful non-Hormuz optionality, but not unlimited export flexibility.

This affects trading decisions in at least four ways.

First, Murban and other UAE-linked barrels may deserve a lower physical disruption premium than Gulf grades without a bypass route, assuming Fujairah remains operational.

Second, the value of ADCOP headroom rises nonlinearly when Hormuz risk increases. The last 500,000 barrels per day of available bypass capacity can become more valuable than the first 500,000 barrels per day in a stressed market.

Third, Fujairah risk needs to be monitored as a separate node. If Fujairah is disrupted, the market should not treat ADCOP capacity as fully available.

Fourth, freight and bunker signals can move faster than crude differentials. Tight VLSFO availability or rising bunker premia at Fujairah may reveal operational stress before crude benchmarks fully price it.

This affects trading decisions in at least four ways.

First, Murban and other UAE-linked barrels may deserve a lower physical disruption premium than Gulf grades without a bypass route, assuming Fujairah remains operational.

Second, the value of ADCOP headroom rises nonlinearly when Hormuz risk increases. The last 500,000 barrels per day of available bypass capacity can become more valuable than the first 500,000 barrels per day in a stressed market.

Third, Fujairah risk needs to be monitored as a separate node. If Fujairah is disrupted, the market should not treat ADCOP capacity as fully available.

Fourth, freight and bunker signals can move faster than crude differentials. Tight VLSFO availability or rising bunker premia at Fujairah may reveal operational stress before crude benchmarks fully price it.

Practical implications for logistics operators

For logistics operators, ADCOP and Fujairah matter because they influence vessel routing, refuelling strategy and port-call risk.

A shipping desk should not ask only whether Hormuz is open or closed. It should ask:

- Is Fujairah loading normally?

- Are bunker stems available at acceptable lead times?

- Are war-risk underwriters changing terms?

- Are vessels avoiding the Gulf and switching to alternative bunkering hubs?

- Is congestion building at Fujairah, Khor Fakkan, Sohar or Singapore?

- Are cargo owners changing laycans, nominations or delivery basis?

In a normal market, Fujairah is an efficient hub. In a stressed market, it can become both a solution and a bottleneck.

The core conclusion

ADCOP is one of the most strategically valuable pipelines in the global oil market because it gives the UAE a direct crude export route to Fujairah outside the Strait of Hormuz.

But the market should avoid two simplistic claims.

The first false claim is that the UAE no longer needs Hormuz. That is too strong. ADCOP provides partial crude export resilience, not complete energy independence from the Strait.

The second false claim is that ADCOP capacity alone determines export security. That is also too narrow. The real system includes upstream production, crude gathering, pipeline pumping, Fujairah storage, terminal loading, bunker fuel availability, vessel access and insurance.

For commodity traders and logistics operators, the correct way to model ADCOP is as a physical option with hard capacity limits. Its value rises sharply during Hormuz stress, but that value depends on whether Fujairah remains operational and liquid.

In the current market, ADCOP should be on every oil and freight risk dashboard.

But the market should avoid two simplistic claims.

The first false claim is that the UAE no longer needs Hormuz. That is too strong. ADCOP provides partial crude export resilience, not complete energy independence from the Strait.

The second false claim is that ADCOP capacity alone determines export security. That is also too narrow. The real system includes upstream production, crude gathering, pipeline pumping, Fujairah storage, terminal loading, bunker fuel availability, vessel access and insurance.

For commodity traders and logistics operators, the correct way to model ADCOP is as a physical option with hard capacity limits. Its value rises sharply during Hormuz stress, but that value depends on whether Fujairah remains operational and liquid.

In the current market, ADCOP should be on every oil and freight risk dashboard.

FAQ

What is ADCOP?

ADCOP is the Abu Dhabi Crude Oil Pipeline, also known as the Habshan-Fujairah pipeline. It carries crude oil from ADNOC Onshore facilities in Abu Dhabi to the Fujairah oil export terminal on the Gulf of Oman.

Does the UAE have a pipeline that bypasses the Strait of Hormuz?

Yes. The UAE can bypass the Strait of Hormuz for part of its crude exports using ADCOP, which connects Abu Dhabi to Fujairah outside the Strait.

What is ADCOP pipeline capacity?

The IEA says ADCOP’s original nameplate capacity is 1.5 million barrels per day, with reported current capacity close to 1.8 million barrels per day. The Port of Fujairah also refers to 1.8 million barrels per day.

Can ADCOP replace the Strait of Hormuz?

No. ADCOP is strategically important, but it cannot replace the Strait of Hormuz for the wider Gulf. The IEA estimates that nearly 20 million barrels per day of oil moved through Hormuz in 2025, far above the available bypass capacity.

Where does the ADCOP pipeline end?

ADCOP ends at Fujairah, a major oil export, storage, blending and bunkering hub on the Gulf of Oman.

Who owns ADCOP?

According to ADNOC, Abu Dhabi Crude Oil Pipeline LLC is 100% owned by ADNOC.

Is BlackRock an owner of ADCOP?

ADNOC states that ADCOP is 100% owned by ADNOC. BlackRock participated in a separate ADNOC oil pipeline infrastructure investment structure, but public ADNOC materials should not be read as proof that BlackRock owns ADCOP directly.

Why does Fujairah matter to oil traders?

Fujairah matters because it is the endpoint of ADCOP, a major oil storage and blending hub, and one of the world’s largest bunkering hubs. If Fujairah is constrained, ADCOP’s practical export value falls.